Flat Rents and Record Vacancies In Multifamily

Canada’s Apartment Market Is Still Healthy… But It’s Starting to Bend

Listen to the full episode here:

Multifamily fundamentals in Canada are no longer surging.

They’re stabilizing.

And in some markets, they’re softening.

These charts come from the Yardi Quarterly Report - You can get it here: https://info.yardi.com/multifamily-market-reports-for-canada

The Q1 2026 national multifamily data shows a rental market that remains structurally undersupplied — but increasingly fragile. Rent growth is slowing. Vacancy is rising. Demand is weakening in key provinces. And for the first time in years, new lease rents are falling in major cities.

This is not a crash.

But it is a regime shift.

Let’s break it down.

The Macro Backdrop: Slower Growth, Fewer Renters

Canada’s economy stabilized in late 2025 after tariff uncertainty from the U.S. faded. Roughly 90% of exports remain tariff-free, and consensus GDP growth for 2026 sits between 1.0–1.5%.

That’s not recessionary.

But it’s below capacity.

The labour market reflects that softness:

226,000 jobs were added in 2025

Unemployment ended the year at 6.8%

Youth unemployment hovered near 15%

Student unemployment hit 18%

That last point matters.

Young adults drive rental demand. When youth unemployment rises, household formation slows. People double up. Or stay home longer.

At the same time, population growth has collapsed.

Canada’s population is expected to grow by just 0.2% in 2025 — the smallest increase in decades. The country is sharply reducing non-permanent residents, with outflows of international students and temporary workers accelerating.

Less population growth + weaker youth employment = softer apartment demand.

That’s the key shift heading into 2026.

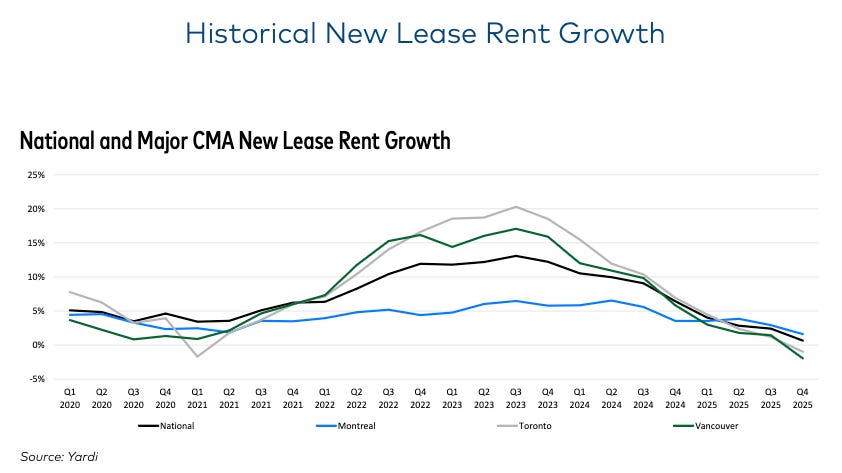

Rent Growth Is Slowing — Fast

National in-place rent rose just $9 in Q4 2025 to $1,746.

That’s the smallest quarterly increase in over four years.

Annual rent growth fell to 3.2%, down 70 basis points from the prior quarter.

To put that in perspective:

2022–2023: double-digit rent growth

2024: mid-single digits

Late 2025: low single digits

New lease growth: nearly flat

And here’s the real story:

New lease rent growth nationally is just 0.7%.

That’s down from:

6.4% one year ago

2.4% last quarter

In several major markets, new lease rents are actually falling.

Negative new lease growth:

Toronto: -1.0%

Kitchener–Waterloo: -2.7%

Hamilton: -0.2%

Calgary: -4.2%

When lease-over-lease rents turn negative, that’s the market signaling supply is starting to meet — or exceed — marginal demand.

This doesn’t mean overall rents are collapsing. Renewal rents are still growing around 2.8%. But pricing power has clearly weakened.

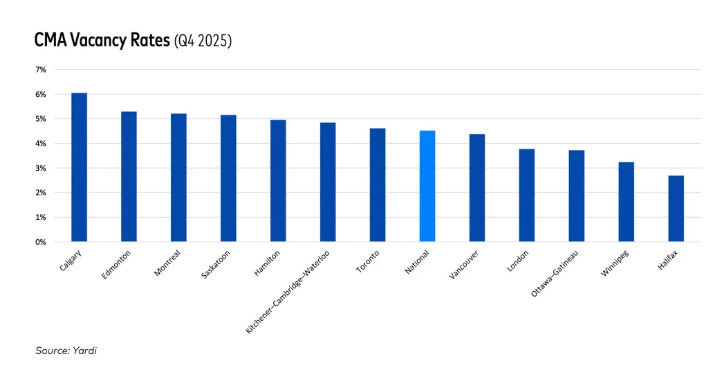

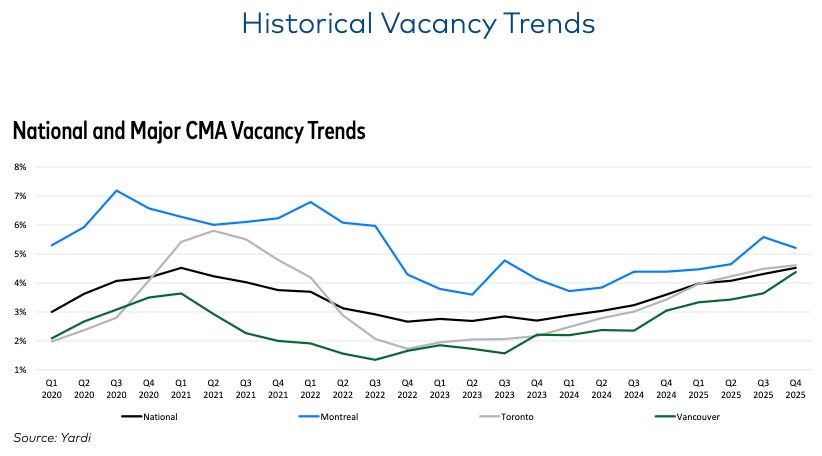

Vacancy Has Hit a Post-Pandemic High

The national apartment vacancy rate is now 4.5%.

That’s:

Up 90 basis points year-over-year

The highest level since 2020

Some markets are materially softer:

Calgary: 6.1%

Edmonton: 5.3%

Montreal: 5.2%

Hamilton: 5.0%

Toronto and Vancouver are not immune either. Vacancy has climbed meaningfully compared to the ultra-tight conditions of 2022–2023.

The market is not distressed.

But it is loosening.

Turnover is rising to 25.5%. Tenants are moving more frequently. Incentives are reappearing in some submarkets.

This is a normalization phase.

Supply Is Still Coming

Despite softening rents, construction hasn’t stopped.

Through the first three quarters of 2025:

122,000 apartment units were started

Apartment starts are up 8.1% year-over-year

Apartments now represent 68.5% of all housing starts

That’s historically high.

Deliveries in major cities were mixed:

Vancouver: +36.5% completions

Edmonton: +8.5%

Toronto: -8.3%

Montreal: -11.1%

Ottawa: -14.7%

The pipeline remains heavy in certain metros, particularly where population growth has slowed.

That’s why we’re seeing divergence.

Alberta: A Tale of Two Cities

One of the most interesting splits right now is inside Alberta.

Edmonton

New leases: +0.9%

Renewals: +1.7%

Vacancy: 5.3%

Calgary

New leases: -4.2%

Renewals: -3.3%

Vacancy: 6.1%

Calgary absorbed massive population growth in 2022–2023. Developers responded aggressively.

Now supply is hitting at the same time demand is moderating.

This is what late-cycle rental dynamics look like.

Ontario Is Softening

Ontario faces a unique mix of pressures:

Outmigration to other provinces

Fewer international students

Condo investors renting unsold units

Slower job growth

Toronto’s apartment market is being cushioned somewhat by office absorption — 2.7 million square feet in 2025 — driven by banks and major employers.

But new lease rents are still negative.

That’s a shift.

Bachelor Units Are Weakest

Smaller units are seeing the most pressure.

Vacancy for bachelor units is materially higher in several cities, with some submarkets seeing double-digit vacancy.

That aligns with youth unemployment and slower international student growth.

1-bed and 2-bed units remain more stable.

3-bed units remain relatively tight due to limited supply.

Expenses Remain Elevated

While rent growth slows, expenses remain high.

National annual operating expenses:

$8,004 per unit

Ontario: $8,822

Alberta: $8,044

Margin compression is becoming a real conversation.

If revenue growth slows and expenses stay elevated, underwriting assumptions must adjust.

So What Does This Mean?

Three key takeaways:

1. This is not a collapse.

Canada remains structurally undersupplied. Occupancy is still solid by historical standards.

2. But the easy rent growth is over.

The demand shock from immigration and post-pandemic household formation has faded.

3. Markets will diverge.

Markets with rapid supply growth and slowing migration will soften first. Markets with constrained supply and stable employment will hold up better.

The Big Picture

The Canadian apartment market is still healthy.

But it is no longer red-hot.

We’ve shifted from:

Scarcity-driven rent spikes

toNormalized, income-constrained growth.

2026 looks like a year of digestion.

Not distress.

Not boom.

Stabilization.

And for investors, that means discipline matters again.

Underwrite conservatively.

Focus on fundamentals.

Watch population flows.

And pay attention to submarket-level supply.

The era of “rents only go up” is over.

The era of careful capital allocation is back.