Lessons From Past Recessions

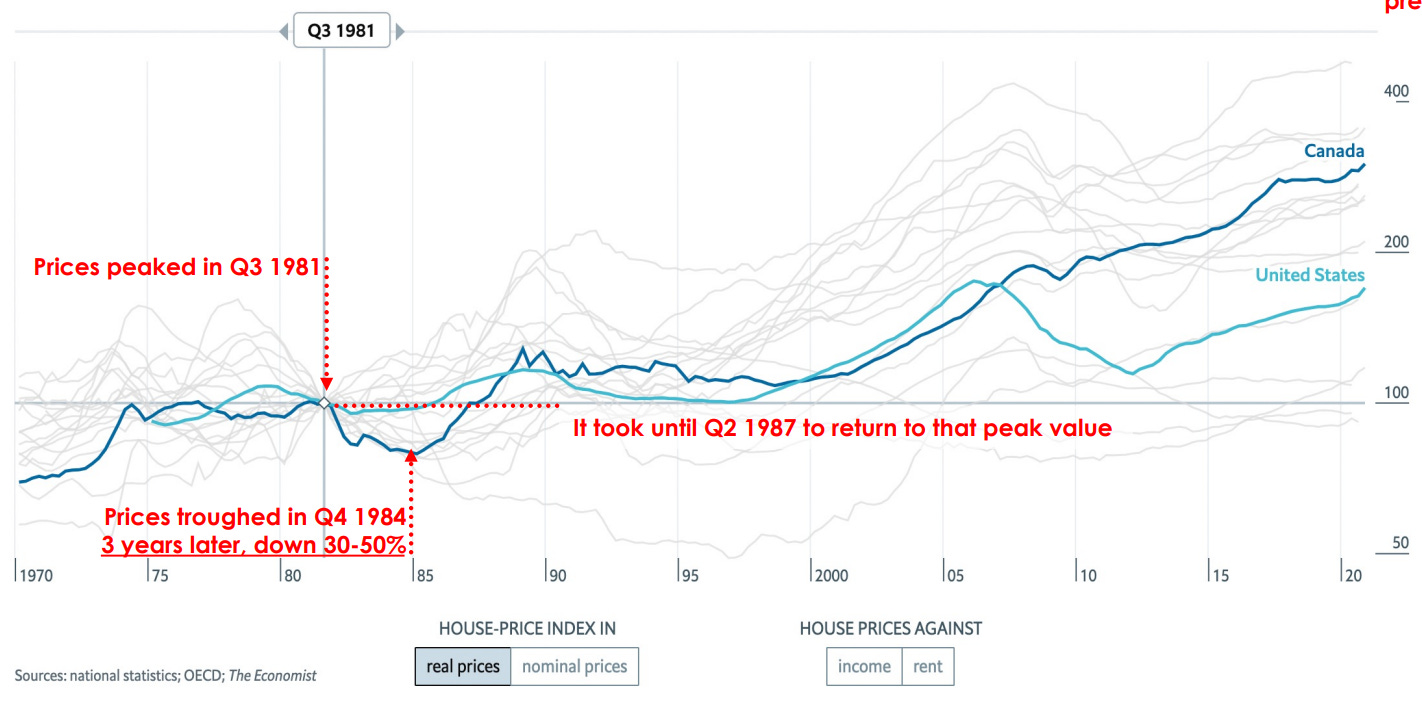

In 1981, the Canadian Consumer Price Index (CPI) was up an astounding 12.47%. The rate had been consistently rising since 1976. Over that period, the Bank of Canada tripled the prime rate of interest. This situation made housing extremely unaffordable across the country. In fact, the average mortgage rate in the 80s was comparable to a credit card rate today: 19.7%.

However, 1981 marked the peak for everything. Canada was officially in a recession from the second half of that year. Disinflation set in which encouraged the Bank of Canada to start rapidly cutting interest rates. Meanwhile, house prices peaked in the third quarter of 1981 and would drift 30% to 50% lower until the fourth quarter of 1984.

Key lesson: Rapid rate hikes successfully broke the back of inflation. House prices didn’t drop until disinflation set in.

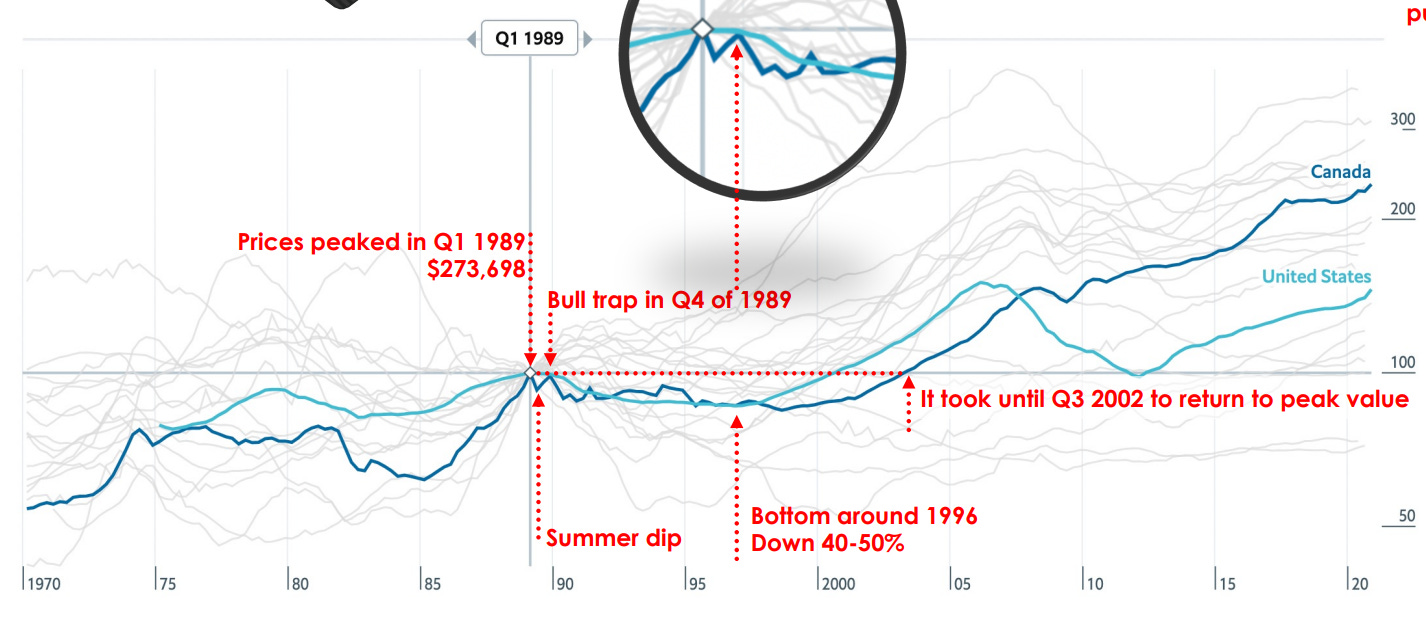

In 1991, CPI inflation was 5.6% - the highest rate in seven years. Yet again, the Bank of Canada deployed its most potent tool: rate hikes. It’s worth noting that inflation surged from 3.9% in 1986 to 5.6% in 1991, but the prime rate was doubled over this period. Policymakers, it seems, had learned their lesson from the previous cycle and were more aggressive this time.

Yet again, the peak of inflation and interest rates marked the peak for real estate prices. House prices across Canada fell 40% to 50% from 1989 to 1996.

Key lesson: Front-loading interest rate hikes capped inflation sooner and caused a deeper dip in house prices.

The Global Financial Crisis or GFC of 2008 was an external shock from the U.S. Inflation and rates were not in an upward trend before this crisis. But the Federal Reserve cut interest rates sharply to deal with this crisis which compelled the Bank of Canada to break through its rate floor too. By 2010, the prime rate was near 0%.

It helps to think of this period as a counter-cycle. Instead of rapid inflation creating the need to raise interest rates and tame demand, an external shock had destroyed demand which created deflation and convinced policymakers to lower rates.

This event created the Canadian real estate boom that is just ending now. The average home price surged from $300k in 2009 to $735k today. That’s a compounded annual growth rate of 17.5% over 14 years.

Key takeaway: Canada’s rate cuts created a prolonged and unsustainable housing boom.

Today’s downturn looks strikingly similar to traditional cycles we experienced in the 1980’s and 90s. There’s an energy crisis and rising inflation. The Bank of Canada is deploying rate hikes in an effort to curb demand and tame inflation bond yields.

Based on our lessons from past cycles, it’s likely that home prices will continue to descend until inflation has bottomed. This phase could take several years. Especially given how elevated valuations were during the recent boom. There’s no guarantee that the ongoing downturn will resemble what we’ve seen before. But so far the trend seems to hold up and it’s worth keeping an eye on. It could present opportunity for new buyers or for those looking to make a move on the housing ladder