The Price You See Is No Longer the Real Price

Price Discovery in Canada’s New Construction Market Is Moving in Buyers’ Favour

Listen to the full episode:

So, I was quoted in an article with the heading “Will HST cut on new homes save buyers money? Early look finds 78% of prices are the same or higher” but the truth is… the majority of new homes are cheaper for buyers today than they were on March 29th, 2026 (a day before the GST/HST rebate came into place). My team analyzed this in detail at valery.ca, and we found that more builders are dropping prices than increasing, and those who haven’t dropped yet are technically cheaper to buyers. Even the properties that increased price, for the most part, did so to an extent that it was still fully-offset by the GST/HST rebate:

The Canadian Housing Market Is Getting Cheaper, Even If the Listings Don’t Show It Yet

Something strange is happening in the Canadian housing market right now. Prices are not crashing, but almost everything is getting cheaper, and most people do not seem to see it yet. The reason is simple: the number you see on a listing is no longer necessarily the real price.

That is the part that makes this market so easy to misread. Headlines say the market is stabilizing. Prices look flat. Buyers are still cautious. Sellers are still stubborn. Builders are still trying to protect comps. On the surface, it looks like nothing has really changed. But underneath the listing price, one of the biggest affordability shifts in years may already be happening.

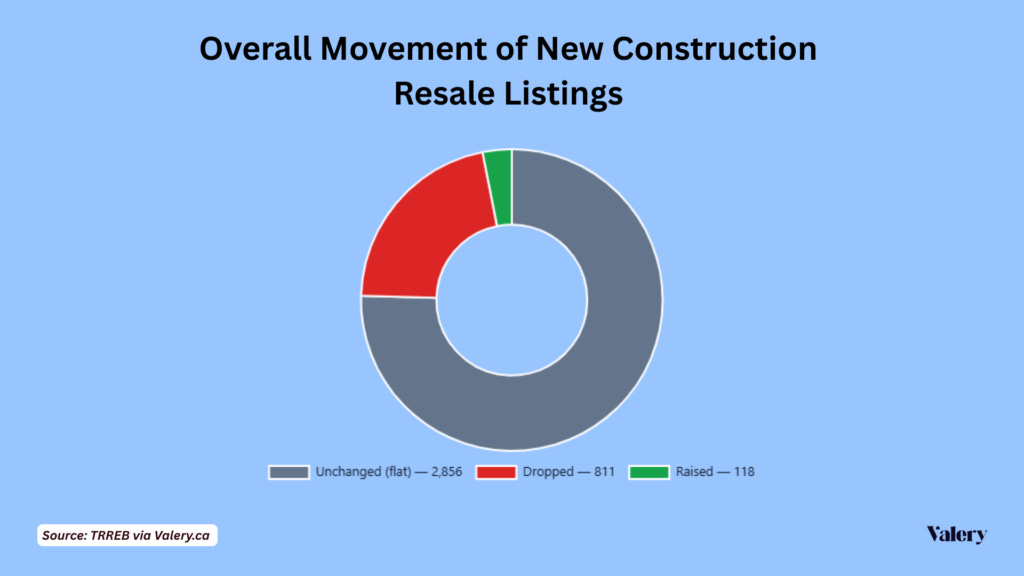

This is especially true in the new construction market. We looked at more than 1,000 floor plans across roughly 100 projects, along with nearly 4,000 active listings across Canada, to understand how builders are responding to the expanded GST/HST rebate environment. The results were pretty clean: about 22% of units had price cuts, about 70% had no listed price change, and only about 8% had increased.

That matters because it cuts against one of the loudest narratives around the rebate. A lot of people assumed builders would simply raise prices and absorb the buyer benefit. In theory, if the government gives buyers a tax break, builders could just increase the sticker price and capture the value themselves. But that is not what the data appears to show. Price cuts are happening more than two and a half times as often as price increases. That is not just noise. That is direction.

The important point is not only that prices are being cut. It is also that the cuts appear broader and deeper than the increases. Builders are not uniformly raising prices into the rebate. Many are cutting. Many are holding. Very few are increasing. This does not mean the market is crashing. It also does not mean the market is recovering. It means the market is going through price discovery. Everyone is trying to figure out what things are actually worth.

The real story, though, is not the 22% of units that got visibly cheaper. The real story is the 70% that did not change, because many of those units may have effectively become cheaper too.

That sounds contradictory, but it comes down to the mechanics of the expanded GST/HST rebate. The policy is meant to improve affordability for new homes. Broadly, buyers can receive a full rebate under $1 million, a partial rebate up to $1.5 million, and in Ontario the maximum benefit can be roughly $130,000. Outside Ontario, the GST portion still matters, but Ontario is where the combined GST/HST impact can be especially large.

The key detail is that the sticker price may not move even when the buyer’s effective cost does. A $900,000 new condo may still show up as a $900,000 new condo. On paper, nothing changed. But if the buyer is eligible for a meaningful rebate, the actual economic cost of that home may have dropped by tens of thousands of dollars. In some Ontario examples, that can look like a near 10% improvement in effective affordability, even though the listing price looks flat.

This is why the market is so confusing right now. If you only track headline prices, you may conclude that nothing is happening. But if you track the buyer’s actual net acquisition cost after rebates and incentives, a huge share of the market may already be cheaper.

That is what I would call a stealth discount market. The discount exists, but it does not always show up where people are trained to look. Most buyers look at the listing price. Investors should be looking at the net cost after rebates, incentives, closing mechanics, and financing realities. Those are not the same number anymore.

There is a catch, though, and it matters. A rebate is valuable, but it is not always the same thing as an instant price reduction. Depending on how the transaction is structured and where the policy process stands, some buyers may still need to pay the full price at closing and receive the rebate later. That means buyers still need enough cash, financing flexibility, and confidence that the rebate will come through.

That is one of the reasons demand has not suddenly snapped back. A cheaper home does not automatically create a qualified buyer. Buyers still need liquidity. They still need income. They still need borrowing capacity. They still need confidence. After the last few years of higher rates, higher living costs, tighter financing, and weaker sentiment, affordability is not only a math problem. It is also a confidence problem.

That is the paradox of this market. Buyers asked for cheaper prices. Now parts of the market are getting cheaper, but many buyers are still hesitant. That tells you the issue is not only price. It is sentiment, liquidity, and trust in the market.

Builders are dealing with their own version of the same problem. Right now, many of them seem to be stuck in a game theory problem. Imagine two builders with similar projects in the same area, competing for the same buyers. If Builder A cuts prices by 10%, they may sell faster, but they also risk resetting the entire market lower. Appraisals may come in lower. Buyers in nearby projects may start demanding discounts. Existing purchasers may get upset. Other builders may be forced to follow.

Builder B then faces the same choice. If they hold prices, Builder A may absorb the demand. If they cut prices too, the whole market may reprice lower. So both builders hesitate. Nobody wants to be the first one to officially slash prices and reset the comp set.

Instead, many builders hold headline pricing, offer incentives, negotiate quietly, or let the rebate do some of the work. That is why so much pricing appears unchanged even though affordability is improving. The market is in a temporary truce. Builders are trying to protect comps. Buyers are waiting for better deals. Inventory is building. Financing pressure is rising. Everyone is waiting to see who blinks first.

The problem is that this kind of truce is unstable. Builders can hold prices for a while, but they cannot hold forever if inventory keeps building and sales stay slow. Carrying costs are real. Debt is real. Construction financing is real. Project timelines are real. At some point, unsold inventory becomes a problem that needs to be solved.

That does not necessarily mean a crash. It does not mean every project suddenly cuts prices overnight. But it does mean the current market structure is under pressure. If sales remain weak, more builders will have to choose between protecting price and generating absorption. In a hot market, builders can protect price. In a slow market, absorption starts to matter more.

For investors, this is where the opportunity starts to show up. The mistake right now is looking only at sticker prices. That is the old way of reading this market. In this environment, you need to look at the listed price, the builder incentive package, the buyer’s rebate eligibility, the closing mechanics, and the net cost after everything is accounted for. That final number is the only number that really matters.

A project that looks expensive at first glance may be much more competitive after rebates and incentives. A project that looks unchanged may actually be meaningfully cheaper. A project with a small price increase may still be effectively discounted if the rebate more than offsets the increase. This is a market that rewards people who do the math.

The opportunity is not obvious because it is hidden in the gap between headline pricing and real pricing. That gap is where investors should be looking. Not every deal is good. Not every market is attractive. Not every builder incentive is meaningful. But the market is clearly becoming more negotiable, and the people who understand the difference between the sticker price and the real price are going to see that before everyone else does.

The Canadian new construction market is getting cheaper. Not everywhere. Not equally. Not always visibly. But meaningfully. Price cuts are happening more often than price increases. Rebate-driven affordability improvements mean many unchanged listings may still be effectively cheaper. Builders are caught between protecting comps and moving inventory. Buyers are still cautious because liquidity and confidence remain tight.

This is not a clean recovery. It is not a crash. It is a repricing process.

And in a repricing process, the listed price is only the starting point. The real deal is what happens after the math.