The un-bubbling of Canadian Real Estate

UBS no longer considers Canada to be at risk of a housing bubble.

We’re still “overvalued” by UBS standards, but no longer at risk of a bubble.

Inflation is up. Bond yields are up. Power of Sales are up. Fixed mortgage rates are up.

House prices might be the only thing not going up.

First things first - UBS no longer considers Canada to be at risk of a housing bubble. The Market shed risk as a result of falling prices and rising incomes, UBS considers the bubble to be “deflating”.

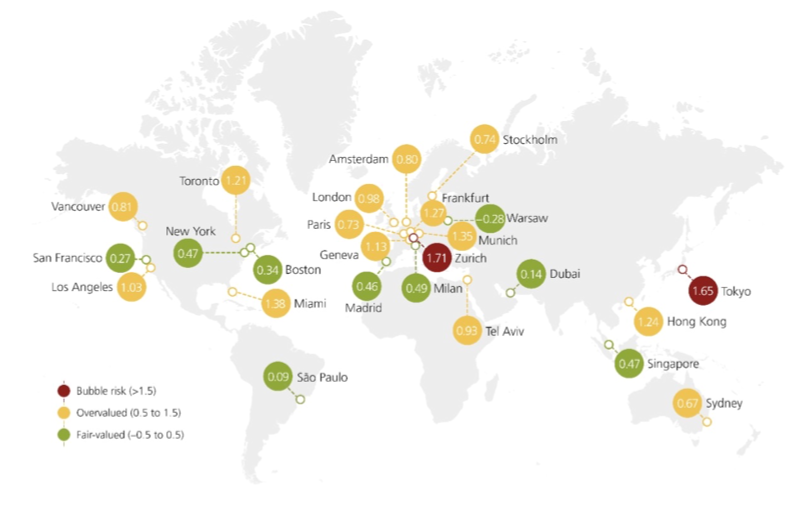

UBS ranks cities based on a number of criteria:

Price to income

Price to rent

Risk of overbuilding

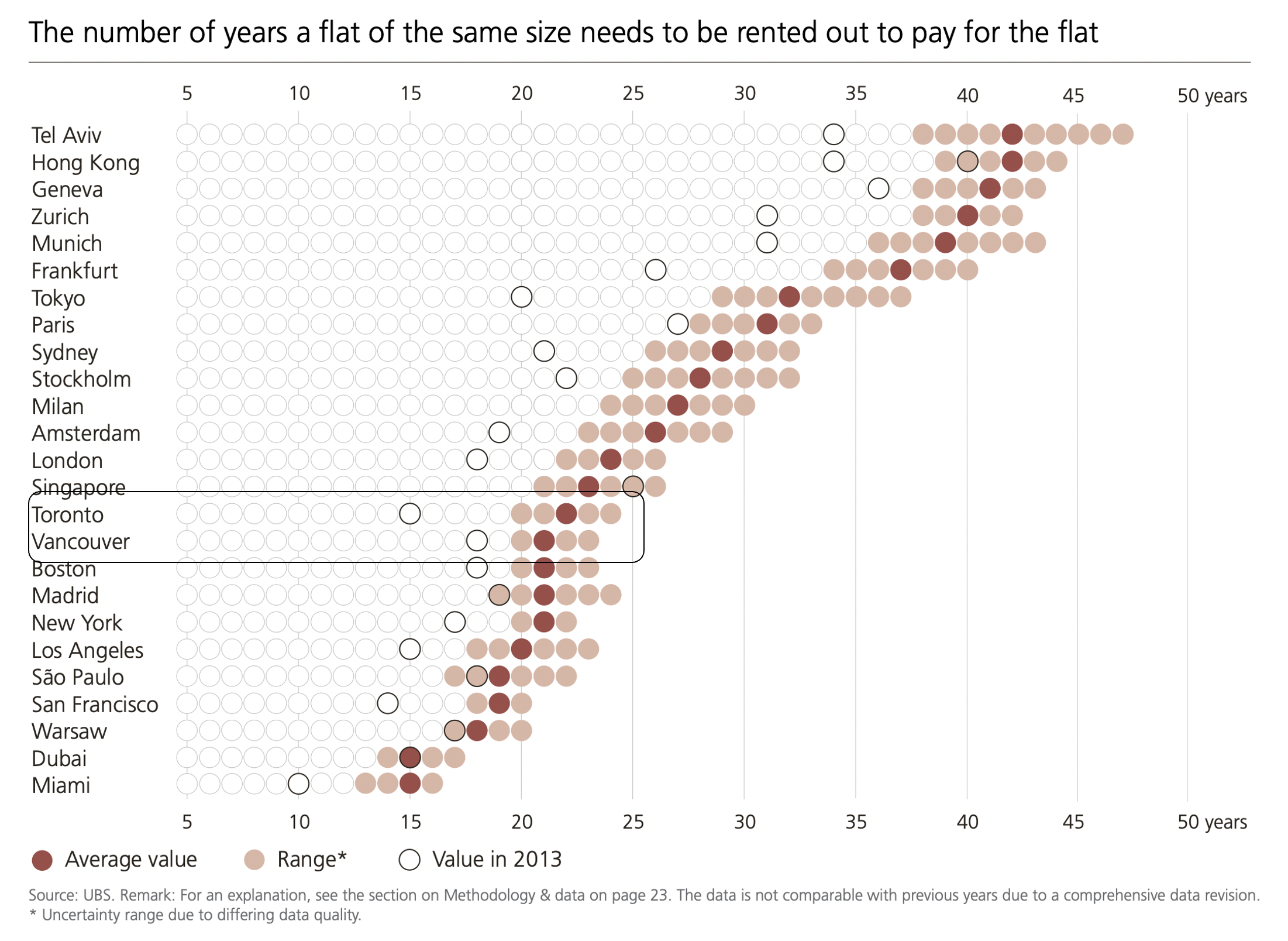

When looking at the price-to-rent statistic, Toronto and Vancouver actually seem to stack up quite nicely against our fellow “world class cities” seen in the UBS index. This chart shows the number of years a 650 sf apartment in the city centre would need to be rented to pay for itself:

Indicators of distress

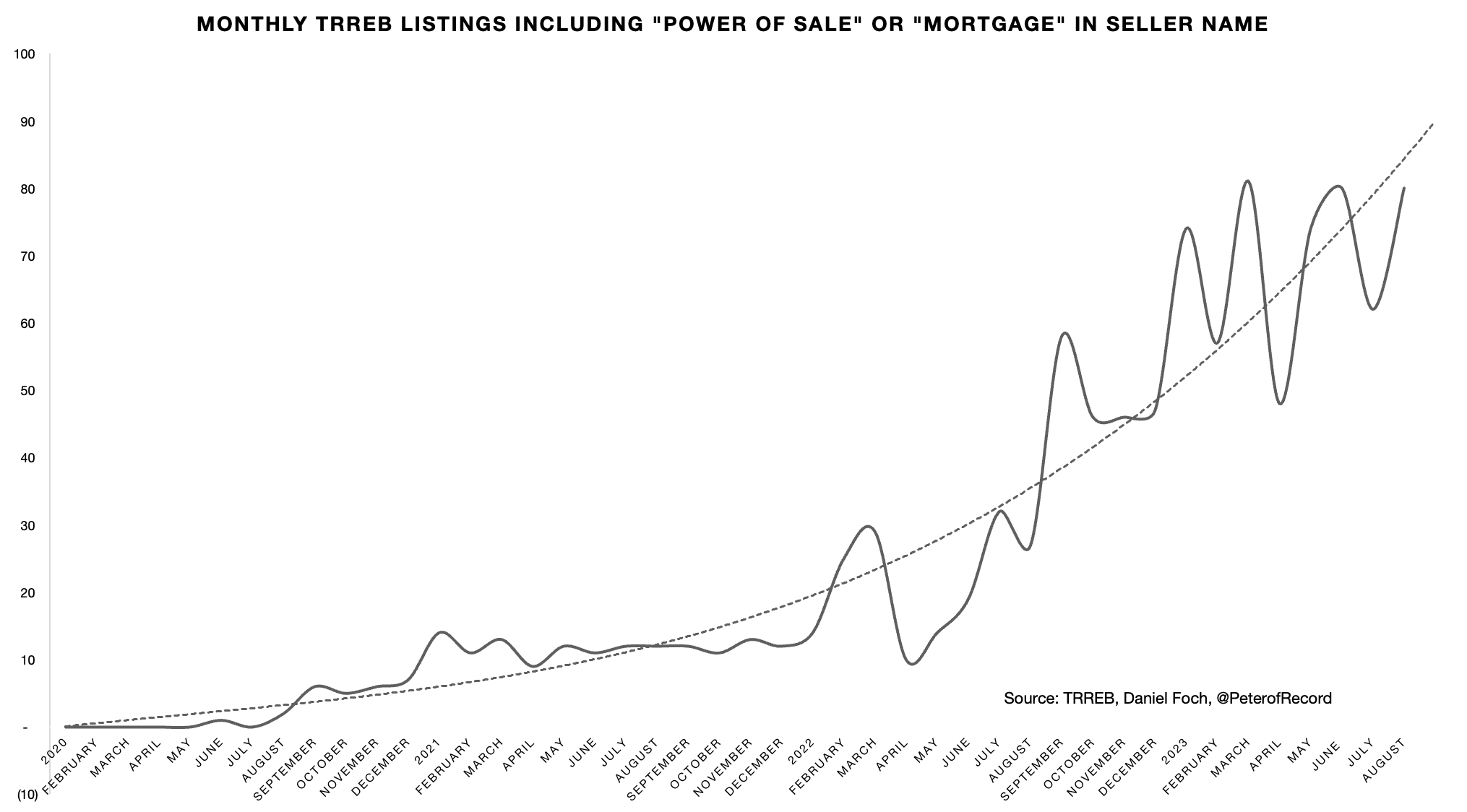

I presented these charts at Veritas’ “The Squeeze” conference to an audience of mostly bankers. I’ve been looking for signs of distress within the supply side. We know that mortgage delinquencies are at record lows based on data from CBA - The Canadian Banker’s Association, and CMHC - The Canadian Mortgage and Housing Corporation.

My challenge with this data is that banks are only required to report mortgages that are more than 90 days delinquent. During this 90-day period, a prudent lender would exercise their power of sale, the most common forced sale process used in Canada when a homeowner fails to repay their mortgage, and the property would likely have already appeared as a listing on the MLS.

As a result, we’ve seen substantial increase in power of sale listings, creating an alarming trend as we head toward a recession in Canada. Could this be a leading indicator on the direction delinquencies could head?

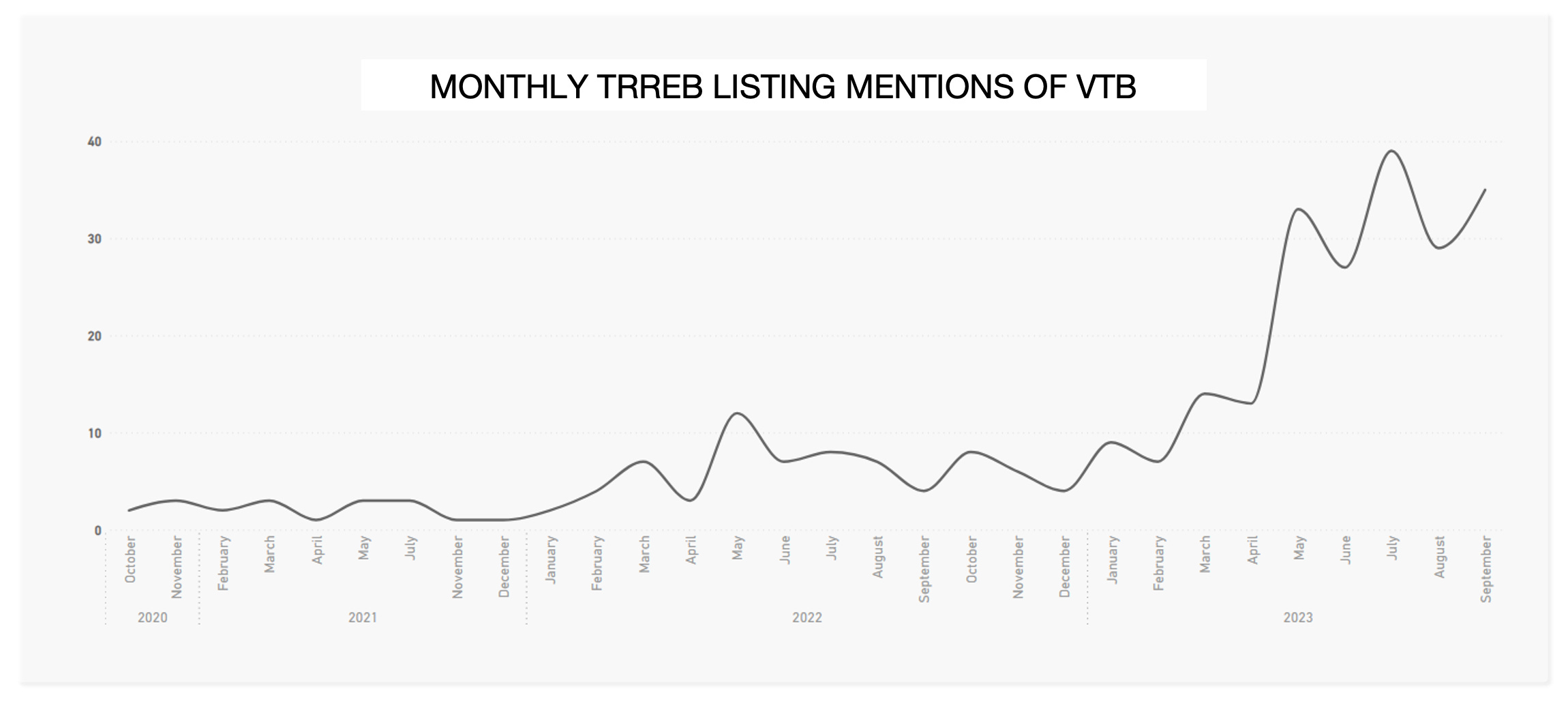

Seller financing

A similar trend to Power of Sales is occurring with sellers offering vendor-take-back (VTB) mortgages at a record rate. Sellers are pulling out all the stops to sell their assets in today’s market in an attempt to secure Q1 pricing.

The increase in VTB transactions was a hallmark of distress and creativity in the 1990’s downturn. Buyers and sellers worked to keep the market moving when credit was in contraction, much like we’re seeing today.

This trend creates a unique opportunity for a win-win between opportunistic buyers who are limited by interest rates, and for sellers who have a preference to being liquid in today’s market.