This episode may upset some realtors

The most important shift in Canadian real estate is not robots replacing realtors. It is AI quietly rewiring search, underwriting, valuation, construction, and operations.

Listen to the full episode:

The Intelligence Shift: AI Isn’t Replacing Real Estate. It’s Rewiring It.

This post is probably going to upset some Realtors.

Not because AI is about to replace every agent, appraiser, mortgage broker, lawyer, developer, or tradesperson in one clean sweep.

It is more uncomfortable than that.

AI is not replacing real estate. It is rewiring the parts of real estate that were always information businesses pretending to be relationship businesses.

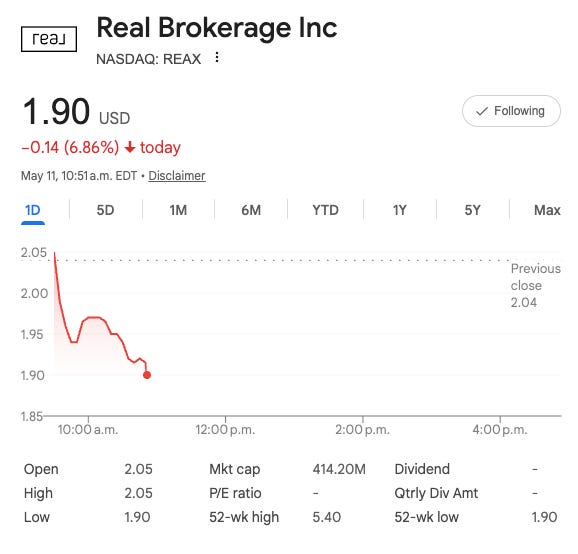

And the clearest signal may be the Real Brokerage / RE/MAX deal.

Real Brokerage announced an agreement to acquire RE/MAX Holdings in a transaction implying an enterprise value of about $880 million. The combined company, expected to be called Real REMAX Group, would have more than 180,000 agents, nearly 8,500 franchisees and offices, operations in more than 120 countries and territories, and pro forma 2025 revenue of roughly $2.3 billion before synergies. RE/MAX shareholders can elect either 5.15 shares of the new combined company or $13.80 in cash, but the cash pool is capped between $60 million and $80 million. Real shareholders are expected to own about 59% of the combined company, while RE/MAX shareholders are expected to own about 41%, subject to closing conditions and approvals.

On paper, it is the perfect old-world-meets-new-world deal.

RE/MAX has the brand, the balloon, the franchise network, the consumer recognition, the global footprint, and the agents.

Real has the cloud brokerage model, the AI narrative, the proprietary software, the lower-overhead operating structure, and the public-market growth story.

But the market reaction tells a more complicated story.

As of May 11, 2026, Real Brokerage was trading around $1.95 and RE/MAX Holdings around $9.99. At that Real share price, the 5.15-share stock consideration is worth about $10.04, far below the original $13.80 headline value and only slightly above where RE/MAX was trading.

That does not mean the deal fails.

It means the market is pricing risk.

Deal risk. Integration risk. Stock consideration risk. Shareholder approval risk. And maybe something bigger: the possibility that putting a tech-forward brokerage and a legacy franchise network together does not automatically solve the structural problem facing both.

Legacy brokerages have distribution but need modernization.

Tech brokerages have software but still need agents, transaction volume, and distribution.

That is the real story.

This is not simply a story about one brokerage buying another brokerage. It is a signal that the old real estate growth model is under pressure.

For years, the model was agent count, transaction volume, cheap credit, rising home prices, and a belief that liquidity would eventually bail everyone out.

Now the industry has to answer a harder question:

What replaces that?

The answer is not “AI replaces Realtors.”

The answer is that AI attacks the information layers of real estate first.

Search. Listing creation. Valuation. Mortgage underwriting. Document review. Due diligence. Project management. Leasing. Asset operations.

Anywhere real estate is really a data problem, a document problem, a workflow problem, or a pattern-recognition problem, AI is coming quickly.

Anywhere real estate is physical, emotional, negotiated, relationship-driven, or dependent on skilled hands in messy real-world environments, AI is much slower.

That distinction is everything.

The brokerage model is becoming a technology distribution problem

The Real / RE/MAX deal matters because it shows both sides of the industry trying to solve each other’s weakness.

RE/MAX has what every tech brokerage wants: distribution. It has agents, franchisees, market presence, consumer awareness, and an international network that would take decades to build organically.

Real has what legacy brokerages want: a modern technology stack, a cloud brokerage structure, an AI-enabled operating story, and the ability to pitch agents on speed, tools, economics, and automation.

The bull case is obvious.

Real pushes its technology through the RE/MAX network. RE/MAX gets a modernization path. The combined company cuts duplicated public-company and back-office costs. Agents get better tools. Franchisees get more productivity. The company gets more data and more opportunities to attach mortgage, title, insurance, lead-gen, and other services to the transaction.

The company itself says it expects about $30 million in annual run-rate cost synergies, largely from shared services, public-company costs, corporate functions, and technology efficiencies.

But the bear case is just as obvious.

What if the problem is not that legacy brokerages lack software?

What if the problem is that the entire brokerage industry is still too dependent on transaction volume, agent count, and commission economics that are already under pressure?

What if distribution without margin is not enough?

What if technology without transaction flow is not enough?

That is why the market reaction matters. The public market is not just asking whether the deal closes. It is asking whether the deal creates value.

And that question applies far beyond Real and RE/MAX.

Every brokerage is about to face the same test.

Can you use AI to make agents more productive, consumers better informed, and transactions less painful?

Or are you just wrapping software around the same old model?

Search and selling are already changing

The most visible layer of AI in real estate is search.

Consumers may not think of property search as AI, but it increasingly is.

Recommendation engines learn what buyers click on, save, ignore, revisit, and share. They infer preferences that buyers may not even be able to articulate. They surface homes that do not perfectly match the original search criteria but may match the buyer’s actual behaviour.

For sellers, the marketing stack has changed even faster.

Listing descriptions can be generated in seconds. Photos can be enhanced. Rooms can be virtually staged. Social ads can be targeted automatically. Leads can be routed, scored, followed up with, and re-engaged by AI.

The boring administrative work around selling a property is being compressed.

That does not make the agent irrelevant.

It changes what the agent has to be good at.

The agent who used to win by controlling access to information is in trouble.

The agent who can interpret information, negotiate effectively, manage emotion, understand local nuance, and guide a client through risk is still extremely valuable.

That is the new division of labour.

AI handles the first draft, the first filter, the first comparison, the first pass.

Humans handle judgment.

Deloitte’s 2025 commercial real estate outlook found that 76% of surveyed commercial real estate organizations were researching, piloting, or in early-stage implementation of AI processes and solutions. Deloitte also found that 81% of respondents identified data and technology as the area where they were most likely to focus spending for the coming year.

In Canada, Statistics Canada found that real estate and rental and leasing businesses planning to adopt AI software rose from 10.9% in Q2 2024 to 18.6% in Q2 2025.

Those are not dominant numbers yet.

But the direction is clear.

Valuation is where AI is powerful — and dangerous

Valuation is the part of the AI story where everyone should be both excited and humble.

Automated valuation models are useful. They are getting better. They can process comparable sales, market trends, property features, rental data, and neighbourhood-level information much faster than any human.

For broad market analysis, they are valuable.

For portfolio screening, they are valuable.

For identifying potential mispricing across thousands of properties, they are valuable.

But for deciding exactly what one specific property is worth on one specific day in one specific neighbourhood, AI still has limits.

Zillow learned this the hard way.

In 2021, Zillow announced it would wind down Zillow Offers, its iBuying business, after concluding that the unpredictability of forecasting home prices exceeded what it had anticipated. The company said the wind-down would include a reduction of approximately 25% of its workforce. Zillow also reported a roughly $304 million inventory write-down in Q3 2021 and expected an additional $240 million to $265 million of losses in Q4 tied mainly to homes it expected to purchase.

That is one of the most important AI lessons in real estate.

The lesson is not that AI valuations are useless.

The lesson is that valuation is not just data.

Valuation is local knowledge, buyer psychology, liquidity, timing, street-by-street nuance, property condition, seller motivation, financing conditions, and market narrative.

An algorithm can be directionally right and financially wrong.

And in real estate, being wrong by 3% can destroy the deal.

That matters even more in Canada, where hyperlocal differences are extreme. A property on one side of a Toronto neighbourhood can behave differently from a property two streets over. A Montreal plex can price differently from a nearly identical building beside it because of layout, tenants, deferred maintenance, zoning potential, or financing constraints.

So the right model is not “AI replaces appraisers.”

The right model is “AI does the first pass, humans handle the exceptions.”

Use AI to narrow the range.

Use human expertise to understand the property.

Mortgages may change faster than brokerage

The mortgage process is one of the most obvious places for AI to create immediate value.

Why?

Because mortgages are full of documents, rules, repetitive checks, income verification, fraud detection, policy matching, and exception handling.

That is exactly the kind of workflow AI is good at.

The clean files get automated.

The messy files get escalated.

The human underwriter does less document chasing and more actual judgment.

In mortgage lending more broadly, STRATMOR Group reported that 38% of lenders were using AI or machine learning for tasks such as document classification and indexing, while 48% were using robotic process automation to streamline tasks like ordering appraisals and credit scores.

In Canada, this is already showing up. CMLS Financial has said it built an end-to-end AI-driven approval process and that about 10% of its loans are currently fully committed using rules-based algorithms. A CMLS executive also framed the goal as eliminating repetitive, low-value tasks so people can focus on product development, training, and complex deal structuring.

Scale AI is also backing a Canadian mortgage-processing project involving Blanc Labs and The Mortgage Trail to automate extraction, classification, and validation of borrower documents such as income statements and bank records.

That is where the mortgage of 2030 starts to look very different.

Pre-approvals become faster.

Document verification becomes faster.

Fraud detection improves.

Rate and product recommendations become more dynamic.

The borrower experience starts to feel less like a multi-week paper chase and more like a real-time financial workflow.

But there is a serious caveat.

AI underwriting can also encode historical bias if the models are trained on biased historical data. If past approvals reflected unequal access to credit, the model can learn those patterns and reproduce them.

So the opportunity is real, but the governance matters.

In lending, speed without explainability is dangerous.

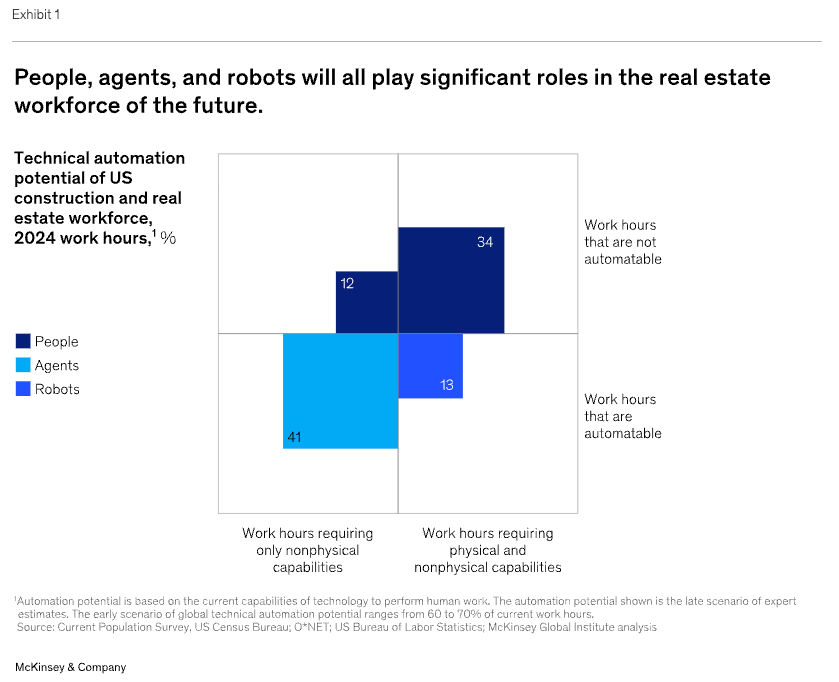

Construction is not immune — but the impact is different

AI in construction is misunderstood.

Most people imagine robots replacing tradespeople on job sites.

That is not the main story.

The main story is design, coordination, estimating, scheduling, procurement, risk management, and building operations.

AI tools connected to building information modelling can help identify conflicts before construction begins. Estimating tools can read drawings, count components, and assist with quantity takeoffs. Scheduling tools can flag conflicts before they become delays. Building systems can optimize energy use in real time.

This matters because construction has a brutal productivity problem.

McKinsey has argued that construction is one of the least digitized sectors in the world and that global construction labour-productivity growth averaged only 1% annually over two decades, compared with 2.8% for the total world economy and 3.6% for manufacturing. McKinsey also estimated that construction productivity catching up with the broader economy could add $1.6 trillion in value, and that action across seven areas — including digital technology, new materials, advanced automation, and reskilling — could boost productivity by 50% to 60%.

Canada already has real examples.

Cadillac Fairview deployed AI-enabled HVAC optimization across major office properties including TD Centre, RBC Centre, Simcoe Place, Toronto Eaton Centre office properties, and Calgary City Centre. The program now covers 12 teams across CF office buildings representing 9.5 million square feet, with reported benefits including reduced utility cost, energy consumption, peak demand, and carbon emissions.

That is not theoretical AI.

That is operational AI inside Canadian real estate assets right now.

The biggest near-term impact in construction is not replacing the worker on site.

It is reducing rework, compressing timelines, improving cost visibility, optimizing buildings, and making scarce labour more productive.

The skilled trades are different

The skilled trades are the part of this story where the “AI replaces everyone” narrative breaks down.

Electricians, plumbers, HVAC technicians, carpenters, welders, and mechanics are not primarily doing abstract information work.

They are working in physical environments that are messy, variable, constrained, and different every time.

Wiring a panel in an old house, diagnosing a plumbing issue behind a wall, installing HVAC in a custom build, repairing equipment in the field — these are physical, context-heavy, judgment-heavy tasks.

AI can help the trades.

It can help with diagnostics.

It can help with quoting.

It can help with scheduling.

It can help with parts identification.

It can help with preventive maintenance.

But it does not easily replace the human being with the tools, the hands, the experience, and the ability to adapt on site.

And Canada has a much bigger issue than AI displacement: not enough tradespeople.

The federal government has said approximately 700,000 skilled trades workers are expected to retire in Canada by 2028.

BuildForce Canada says that in construction alone, roughly 245,100 workers are expected to retire over the next 10 years, while about 237,800 new tradespeople are expected to enter the workforce.

Statistics Canada’s 2026 research on certified journeypersons gives the most useful nuance. It found that the majority of certified journeyperson occupations — including plumbers, carpenters, and welders — appear less exposed to AI-related job transformation than other occupations because their work involves more manual labour. But it also found that about 20.3% of employees in journeyperson occupations were predicted to be at high risk of automation-related job transformation, compared with 12.8% in other occupations, mostly because some tasks are repetitive and machine-automatable.

So the trades are not immune to technology.

But they are much more protected than most white-collar information work.

The practical message for tradespeople is simple:

Learn the tools that make you faster.

Do not ignore AI.

But your core livelihood is not under the same near-term threat as roles built around documents, data entry, content production, or routine analysis.

The full picture: information layers vs. human layers

The best way to understand AI in real estate is to divide the industry into two categories.

The first category is information work.

Search. Valuation. Mortgage underwriting. Document review. Market analysis. Listing creation. Lead routing. Tenant screening. Asset reporting. Scheduling. Energy optimization.

These layers are being rebuilt quickly.

The second category is human and physical work.

Negotiation. Trust. Local judgment. Emotional decision-making. Physical inspection. Skilled trades. On-site construction. Complex problem solving in unpredictable environments.

These layers are much harder to replace.

That does not mean they will not change.

They will.

But they will change through augmentation, not simple substitution.

A good agent with AI becomes faster.

A good investor with AI screens more deals.

A good lender with AI clears clean files quickly and spends more time on exceptions.

A good developer with AI tests more scenarios before committing capital.

A good tradesperson with AI diagnoses faster, quotes faster, schedules better, and spends more time doing the high-value work.

The weak version of AI in real estate is automation for its own sake.

The strong version is leverage.

What this means for agents, investors, and operators

For agents, the value proposition has to move away from “I have access to listings” and toward “I help you make better decisions under uncertainty.”

AI will write the listing description.

AI will summarize the comparable sales.

AI will prepare the first version of the buyer guide.

AI will remind the client about deadlines.

AI will generate the social post.

The agent’s job is to know what matters, what is wrong, what is missing, what is risky, and what the client should do next.

For investors, AI will make deal screening much faster.

But faster screening does not mean better judgment.

The investor still needs to understand financing, zoning, rentability, renovation risk, tenant profile, capex, exit liquidity, and what the market will actually pay for the asset.

AI can tell you what looks like a deal.

It cannot yet reliably tell you what becomes one.

For developers, the advantage is scenario testing.

A site can now be analyzed through multiple lenses: zoning, unit mix, massing, parking, shadow impact, rental demand, construction cost, financing sensitivity, and exit value.

The developer who can test 100 versions of a project before committing capital has an advantage over the developer still underwriting one static version in a spreadsheet.

For operators, AI is moving into the building itself.

Energy optimization, predictive maintenance, tenant communication, leasing workflows, collections, renewals, and reporting are all becoming more automated.

For trades, AI is a productivity tool.

The scarce resource is not software.

The scarce resource is skilled labour.

That scarcity makes the best tradespeople more valuable, not less.

The Real / RE/MAX deal is the opening scene, not the whole movie

The Real Brokerage / RE/MAX deal is important because it shows where the brokerage industry is headed.

Distribution wants technology.

Technology wants distribution.

Both want scale.

Both want more data.

Both want ancillary revenue.

Both want to prove they are not just exposed to transaction volume and agent count.

But the deal also raises the hard question:

Is adding AI and software to a brokerage enough to change the economics?

The answer depends on whether the technology actually reduces friction, improves productivity, and creates value for agents and consumers — or whether it just becomes another layer of tools sitting on top of the same old transaction model.

That is the test for the entire industry.

AI will not save weak business models.

It will make strong operators stronger.

It will expose slow operators faster.

And it will force everyone in real estate to ask a more precise question:

What part of my work is information processing?

What part is judgment?

What part is physical?

What part is relationship?

The information layer is being rebuilt.

The judgment layer is becoming more valuable.

The physical layer is still hard to replace.

The relationship layer still matters, but it has to be backed by better data, better tools, and better execution.

That is the intelligence shift.

Not AI replacing real estate.

AI forcing real estate to become more honest about where the real value is.

[OPTIONAL CTA INSERT]

This is the thesis behind Realist.

Realist is an AI-powered investing platform built specifically for Canadian real estate investors.

Instead of bouncing between spreadsheets, listings, zoning pages, mortgage assumptions, and random calculators, you can tell it what you are looking for — for example, a cash-flowing duplex in Ontario or a multiplex conversion opportunity in Toronto — and it helps surface and analyze deals faster.

The goal is not to replace judgment.

The goal is to give investors a better first pass: cash flow, financing assumptions, upside, multiplex potential, and the key questions to investigate before acting.

In other words, AI should not make the decision for you.

It should make you much better prepared to make the decision.

Closing thought

This is not a technology story.

It is a real estate story.

For decades, real estate was protected by opacity. Information was fragmented. Processes were slow. Documents were manual. Local knowledge was hard to access. Financing was paperwork-heavy. Construction was under-digitized. Brokerage was distribution-driven.

AI attacks all of that.

But it does not attack every layer equally.

The future of real estate belongs to the people who understand where AI creates leverage and where human judgment still matters most.

That is the opportunity.

Not to pretend the industry will stay the same.

And not to pretend software replaces everything.

The opportunity is to build, invest, broker, lend, manage, and operate with a clearer understanding of what is changing underneath the surface.

The old model was built on access.

The new model is built on intelligence.